The Essential Historical Context

In focusing on the post-WWII Western Welfare in the U.S., it is useful to disaggregate this long-term period into two medium-term periods, or phases. Given the cardinal function of labour as the only value and surplus value-producing factor (this is the crucial hypothesis that is supported empirically in Figure 3 below), employment, rather than GDP, has been chosen as the benchmark. The focus is on the productive sectors of the economy because they produce the capital’s vital lymph: value and surplus-value.1 In measuring, prices are deflated because they show the evolution of the value-generation in real terms.

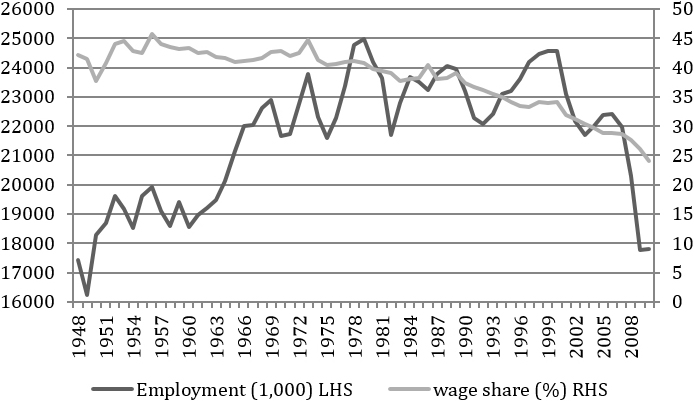

As Figure 1 and Table 1 below show, the first, upward phase in employment goes from 1947 to 1979, the peak year for labour-power; then there is a downward phase that goes from 1980 to 2010. In the upward phase, employment grows from 17.56 million labourers in 1947 to 24.97 million in 1979, a rise of 42.3%. Given the strength of labour, the wage share holds its ground and falls only moderately from 42% in 1947 to 40.8% in 1979, after two all-times peaks in 1956 (45.7%) and in 1973 (44.7%).

In the following downward phase, from 1979 to 2010, employment falls to 17.7 million in 2010, back approximately to the 1947 level, i.e. by -26.9%. The wage share plummets from 40.8% in 1979 to 24% in 2010, i.e. by -41.2%. This indicates the progressive weakening of the US working class.

Figure 1: Employment and Wage Share in the US Productive Sectors

Source: Wages for goods producing industries and are obtained from NIPA tables 2.2A and 2.2B: wages and salaries disbursements by industry [billions of dollars].

Employment in goods producing industries is obtained from: US Department of Labor, Bureau of Labor Statistics, series ID CES0600000001.

Higher employment generates greater total value and new value (as measured by wages plus profits). Table 1 below shows that total value grows by an annual rate of 3.9% in the first period from 1947 to 1979. But that rate falls to 2.9% in the second period, from 1980 to 2010. The slowdown is much more accentuated for new value, from 3.7% in the first period to 1.4% in the second one.

Table 1: Total Value and New Value Percentage Change

| E | Employment % Change | Wage Share | Total Value

Average % Change |

New Value % Change | |

| 1947

1979 |

17.5m

24.9m |

1947-1979

42.3% |

1947: 42%

1979: 40.8% |

1948-1979

3.9% |

1948-1979

3.7% |

| 1980

2010 |

24.2m

17.8m |

1980-2010

-26.9% |

1979: 40.8%

2010: 24% |

1980-2010

2.9% |

1980-2010

1.4% |

Source: Employment and wage share, see Figure 1 above. Total value: Profits are from NIPA tables 6.17A, 6.17B, 6.17C, 6.17D: Corporate Profits before tax by Industry

[Billions of dollars]. In the first three tables utilities (such as the kind you would learn more about here for finding good prices on) are listed apart but in Table 6.17D they are listed together with and cannot be separated from transportation. I have decided to disregard utilities in all four tables.

Constant capital is here the same as fixed capital. The BEA defines fixed assets as “equipment, software, and structures, including owner-occupied housing” (http://www.bea.gov/national/pdf/Fixed_Assets_1925_97.pdf). The data considered in this paper comprise agriculture, mining, construction, and manufacturing (but not utilities, see above). Fixed assets are obtained from BEA, Table 3.3ES: Historical-Cost Net Stock of Private Fixed Assets by Industry [Billions of dollars; yearend estimates].

Wages for goods producing industries and are obtained from NIPA tables 2.2A and 2.2B: wages and salaries disbursements by industry [billions of dollars].

Broadly speaking, the upward phase coincides with the growth of the Welfare State and the downward one with its decline and the emergence of what has been called neo-liberalism. These two periods should be related to their root cause, the movement of the average rate of profit and especially its long-term, tendential fall.

Why Falling Profitability?

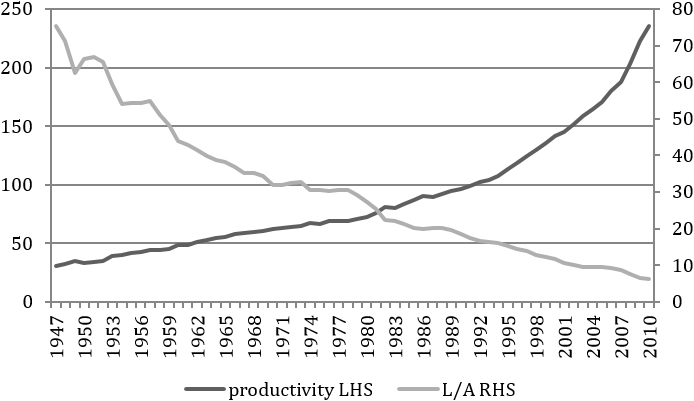

The motor of capitalism’s dynamics is technological development, innovations. But this development is deeply contradictory. To see this, a distinction should be made between labour productivity (output per unit of labour, or O/L) and capital efficiency (labourers per unit of assets, or L/A). The empirical data are clear: when labour productivity rises, the ratio of labour to assets (the L/A ratio) falls.

Figure 2 below shows that the number of labourers working with assets worth one million dollars (deflated figures) drops from 75 in 1947 to 6 in 2010. This is not to say that the mass of labour keeps decreasing. The mass of labour varies with capital accumulation or dis-accumulation (see the upward and the downward phase in Figure 1 above). It is the mass of labour relative to assets (L/A) that decreases tendentially. Figure 2 also shows that the output per labourer (labour productivity) climbs from a deflated $28.9m in 1947 to $231.5m in 2010. In short, figure 2 shows that new technologies are both productivity increasing and efficiency increasing, i.e. labour shedding. This is the basic contradiction inherent in the capitalist economy: an increasing mass of output (use values) contains a decreasing quantity of value.

Figure 2: Labour Productivity and Capital Efficiency in the US Productive Sectors

Source: See Table 1 above.

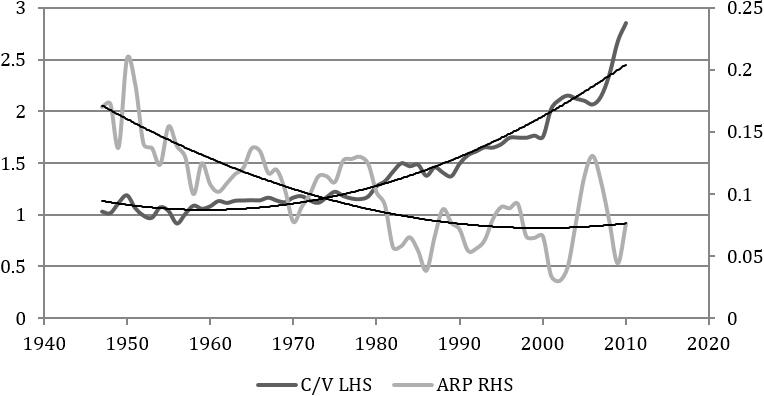

Labour is measured as variable capital (capital spent on wages) and assets as constant capital (capital sent on means of production).2 So, variations in deflated wages indicate variations in the labour-power employed. If, due to technological innovation, labour falls, the new value generated falls. Ceteris paribus surplus value (measured as profits) falls too. Another way to put this is that the ratio of constant capital to variable capital (the C/V ratio in Figure 3 below), also called the organic composition of capital (C/V), rises tendentially over the whole post-war period while the average rate of profit (the ratio of surplus-value – measured as money profits – to the total capital invested) falls tendentially over the same period. The average rate of profit (ARP) falls as the unintended consequence of each capitalist introducing productivity-increasing but labour shedding technological innovations, i.e. as the unintended consequence of technological competition.

Figure 3: Average Rate of Profit (ARP) and Organic Composition of Capital (C/V) in the US Productive Sectors

Source: See Table 1 above.

Given that assets rise relative to labour (the C/V line), if assets created value and surplus-value, the ARP would rise and not fall. Figure 3 substantiates empirically the initial basic assumption that only labour creates value and thus surplus-value.

The fall of the ARP hides a double movement. The productivity of the labourers of the technological leaders rises above that of other capitals, i.e. they produce a greater output (use values) per unit of capital invested than the laggards’ labourers. At the same time, the size of the technological leaders’ labour force is reduced because it is replaced by means of production so that this labour force generates less value and surplus-value. A greater mass of use-values contains a smaller quantity of value. The opposite holds for technological laggards. Due to older techniques, they produce fewer use values per unit of capital with a greater value (because they are produced with a greater labour force). Since unit prices tend to equalize within sectors, the technological leaders sell their (larger) product to other sectors at a price that represents more value than their own value; the technological laggards sell their (smaller) product to other sectors at a price that represents less value than their own value. In this indirect way, the leaders appropriate a share of the surplus-value generated by the laggards.3

Due to the appropriation of value, the technological leaders’ rate of profit rises (even if they generate less surplus value) while both the laggards’ rate of profit and the ARP fall. Thus, a falling ARP indicates that, given a lower total mass of surplus-value produced, the profitability of the innovators rises while the ARP and rate of profit of the technological laggards fall. The latter’s financial situation worsens. As more and more capitalists introduce the new technologies, increasingly less labour is employed and less surplus value is generated. Many capitals go bankrupt while a few prosper, perhaps because these capitals use technologies such as Synario to manage their cashflow and prevent such an event from happening. But for the capitals that go bankrupt, mass unemployment follows. Of course, this is already happening in some industries. Some industries are being more and more digitalized, meaning that there is less need for employees. As this happens, more people become unemployed. Unemployment is negative for economies, as well as forcing many families into poverty. Living in poverty is already a reality for lots of families in America. These families struggle to pay bills, leaving them in uncertainty about their home. No one wants that, so it’s important that families in poverty are actively looking to find the money to pay their bills. There are a lot of different ways to gather some money, perhaps these families should visit https://www.gofundme.com/c/blog/how-to-get-help-with-bills to see some of the methods available to ensure they can pay their bills. Whilst this works now, if mass unemployment strikes, it might not be as easy to gain this money.

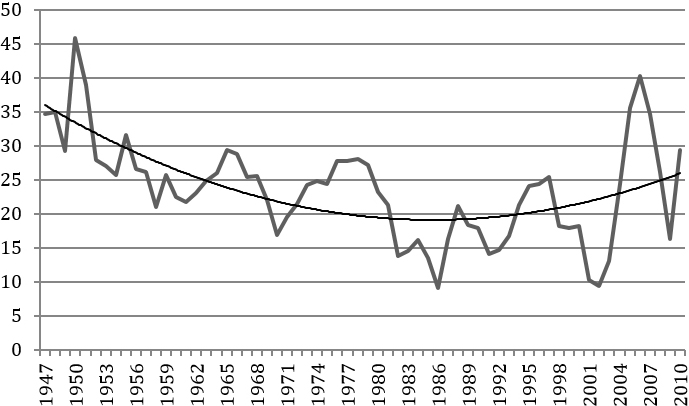

Some authors limit their observation to the 1980-2010 period. In that period, the ARP rises tendentially, as in Figure 3 above. The downward movement of the ARP would appear to be reversed and a new upward tendency begun. However, if set against its historical background, the period from 1980 onwards is a long counter-tendency, an upward movement within the longer 1948-2010 period of downward tendential profitability. This is shown by the trend for the whole period. The objection that a counter-tendency cannot last that long is easily rebutted: a counter-tendency lasts as long as the reason that causes it lasts, in this case, a surge in the rate of exploitation. This is shown in Figure 4 below, where the rate of exploitation is S/V, i.e. the rate of surplus-value to variable capital, or wages.

Figure 4: The Rate of Surplus Value (S/V) in the US Productive Sectors

Source: See Table 1 above.

Thus, the rise in the ARP since the mid-1980s has been due to a tremendous increase in the rate of exploitation, rather than to an increased generation of surplus value per unit of capital invested. Once the increase in the rate of exploitation is factored out, the ARP falls also in the second period (as in Figure 5).

Figure 5: The ARP with S/V Factored Out in the US Productive Sectors

Source: See Table 1 above.

The Rise of the Welfare State

How does the rise of the Welfare State fit into all this? The upward phase has been called the Golden Age of capitalism. The vigorous growth in this phase of employment, total value and new value (relative to the following downward phase), as in Table 1 above, seems to contrast with the fall in profitability in the same period.4 How can the Golden Age and the rise of the Welfare State be reconciled with the persistent fall in average profitability? The answer requires that we step back to the Second World War.

The war produced a massive destruction of capital. In the U.S., it was not a destruction of the physical productive structure and infrastructures. They were unscathed. There was an annihilation of the value contained in the means of destruction (weapons and military apparatus deployed abroad in the war theatre). But this is not the most important aspect. If, as mentioned above, capital is essentially a production relation, the war caused destruction of capital as the capitalist production relation in the civilian sphere and their reconstitution in the military sphere.5

Table 2: Federal Spending and Military Spending, 1941-45, 1940 Constant $Bn

| Federal Spending % Increase | Federal Spending as % of GDP | Defense Spending % Increase | Defense Spending as % of Federal Spending | |

| 1941 | 37.28 | 10.77 | 269.28 | 47.15 |

| 1942 | 132.15 | 21.70 | 259.71 | 73.06 |

| 1943 | 110.64 | 46.59 | 99.46 | 69.18 |

| 1944 | 14.24 | 41.54 | 43.13 | 86.68 |

| 1945 | -0.70 | 41.56 | 2.51 | 89.49 |

Source: Christopher J. Tassava, “The American Economy during World War II,” EH.Net, 2010.

By 1945, almost 90% of federal spending was military spending. The war was a massive conversion of the civilian economy plagued by high unemployment, great excess capacity utilization and falling profitability into a full employment military economy with full capacity utilization, guaranteed realization, high profits and profitability and high levels of saving. High profitability was due basically to three causes. First, before the war, capacity utilization was very low, but as early as June 1941 it had reached 100% in the production of iron and steel and durable goods of all types. Idle assets practically disappeared and with it their dead weight on profitability. The ARP grew on this account.

Second, net fixed investment fell. Using investment index at 2005 prices = 100, investment fell from 4.9 in 1941, to -1.6 in 1942, to -3.2 in 1943, to -1.6 in 1944. Investment rose only in 1945, to +1.3.6 It rose above the 1941 level only in 1946. The organic composition of capital fell and so the ARP grew.

Third, real wages fell. Nominal money wages grew due to near full employment. In 1944, the level of employment had reached 98.8 percent of the labour force and that of the unemployed 1.2 percent. Consequently, “between January 1941 and July 1945 average weekly earnings in the manufacturing industry in the United States rose by 70 percent.”7 However, real wages fell. Here, real wages should not be understood as deflated money wages. They also rose. Rather, they fell in the sense that purchasing power lagged far behind the growth in nominal wages. The reason is that the conversion of a civilian into military industries reduced the supply of civilian goods. This is not to say that living standards were reduced. The standard of living did rise, even if it was not ubiquitous. But production destined for civilian consumption was curtailed, for example, automobiles (which were unobtainable during the war), many non-essential foods, and textiles and clothing.

Higher wages, but with a reduced supply of civilian goods, meant that labour’s purchasing power was greatly repressed. This was achieved by instituting the first general income tax, by prohibiting consumer credit and stimulating consumer saving, principally through the purchase of war bonds. Evidence of the repression of labour’s purchasing power (although labour was not the only purchaser of war bonds) is provided by $167.2 billion of war bonds purchased during the war. This compares with the smaller $136.8 billion revenue provided by taxes. War bonds and taxes covered the war’s total cost of $304 billion.

All told, labour was forced to postpone the expenditure of a sizeable portion of its nominal wages. So, higher nominal wages did not dent profitability because real wages fell. Labour’s purchasing power was frozen. At the same time, the rate of exploitation increased. “The average working week in the United States increased from 38 to 45 hours during the war,” an increase of more than 18%.8 In essence, the war effort was a labour-financed massive production of means of destruction.

With the end of the war, the liberation of labour’s pent-up purchasing power and the reconversion of the military economy into the civilian economy spurred the production first of new means of consumption and then of new means of production.9 Automobilisation (and the suburbanisation it made possible) played a pivotal role.10 The suburbs and the way of life underwent a radical transformation. Greater employment, higher wages, and bigger profits followed and with them a further surge in purchasing power. As Table 3 below shows, the shedding of labour caused by technological innovations – as indicated by the 20% rise in the OCC – was absorbed by the vigorous rate of growth in employment (42.3%, from 1947 to 1979).

Table 3: Employment and Organic Composition of Capital Percentage Change

| E | E % Change | OCC | OCC% Change | |

| 1947

1979 |

17.5m

24.9m |

42.3% | 1.0

1.2 |

20% |

| 1980

2010 |

24.2m

17.8m |

-26.9% | 1.2

2.9 |

142% |

E = employment; OCC = organic composition of capital (C/V).

Source: See Table 1 above.

Federal and military spending fell dramatically.

Table 4: Federal Spending and Military Spending, 1945-50, 1945 Constant $Bn

| Federal Spending % Increase | Federal Spending as % of GDP | Defense Spending % Increase | Defense Spending as % of Federal Spending | |

| 1945 | 1.50 | 41.90 | 4.80 | 89.50 |

| 1946 | -40.40 | 24.80 | -48.60 | 77.30 |

| 1947 | -37.50 | 14.80 | -70.00 | 37.10 |

| 1948 | -13.70 | 11.60 | -28.90 | 30.60 |

| 1949 | 30.50 | 14.30 | 44.40 | 33.90 |

| 1950 | 9.60 | 15.60 | 4.40 | 32.20 |

Source: Christopher J. Tassava, “The American Economy during World War II,” EH.Net, 2010.

The application to the production process of new technologies developed during the war increased labour’s productivity. The war was a wealth of inventions, from the jet plane to ballistic missiles, from atomic energy to computers, from radar to synthetic rubber, just to mention a few. These inventions became the new technologies that flowed over into the civilian economy and became the new material basis of the post-war economy. Synthetic rubber appears in most households and is used in the industrial sector to make hoses, gaskets and belts. To learn more about the applications of rubber, check out HTTPS://WWW.CALIFORNIAINDUSTRIALRUBBER.NET/. As Marx said, “A crisis always forms the starting-point of large new investments. Therefore, from the point of view of society as a whole…a new material basis for the next turnover cycle.”11

The investments in new technologies replaced old fields of investment, old lines of production were completely revolutionized, and new products came into being. New needs had to be created to match the technologically new products. The liberation of purchasing power made the absorption of this new output possible. The civilian economy was jump-started again on a new material basis. This led to generalized welfare, even though it was very unequally distributed (think of the regional, race, and gender disparities). The post-war capitalist society changed beyond recognition while the fundamental laws of its motion remained unchanged.

The Golden Age was based on the reconstitution of civilian capital. In essence, with the coming of the war, capital was first destroyed in the pre-war low-profitability civilian sphere and reconstituted in the high-profitability war economy. Then, after the war, capital was destroyed in the military sphere and reconstituted again as civilian capital within the context of a large-scale, robust, and sustained expanded reproduction. Growth and (very unevenly distributed) welfare first spread from the productive sectors to the rest of the U.S. economy and then it contributed to the growth of the Welfare State in other Western economies. The U.S. Welfare State was born.

The formation of the Welfare State in Europe (in some European nations more than in others) is beyond the scope of this work. Here only a few cursorily remarks will suffice. The role of the Marshall Plan (1948-51) in fostering the European reconstruction and the European Welfare State is a debated question. It probably was modest. From 1948 to 1952, $13.3 billion was granted, only about one-percent of US GDP per year. The economic purpose of the Plan was to create foreign markets for US commodities.12 It did, basically, for large U.S. corporations.13 Some economic historians point out that the reconstruction had already began before the Marshall Plan and that “U.S. assistance hardly exceeded 2.5% of GNP of the recipient countries, and accounted for less than 20% of capital formation in that period.”14

Economists of a Keynesian persuasion argue that federal spending in the U.S. and economic aid to Europe made it possible to finance Keynesian policies and thus to start the long period of prosperity. The heart of this argument is the Keynesian multiplier. Basically, the argument is that investments, employment, and income rise by a multiple of the initial government investment.

The fallacy of the Keynesian multiplier is that it ignores the effect of these investments on profitability. This has been shown in another work.15 Here suffice it to mention that the empirical data do not support the multiplier thesis.

Table 5: GDP, Federal Spending (FS), and Defense Spending DS)

| FS % Growth | GDP % Growth | DS % Growth | DS as % of GDP | |

| 1945 | 1,5 | -0,7 | 40,8 | 37,5 |

| 1946 | -40,4 | -3,4 | -48,6 | 19,2 |

| 1947 | -37,5 | 9 | -70 | 5,5 |

| 1948 | -13,7 | 9,3 | -28,9 | 3,5 |

| 1949 | 30,5 | -0,7 | 44,4 | 4,8 |

| 1950 | 9,6 | 9 | 4,4 | 5,0 |

Source: Christopher J. Tassava, “The American Economy during World War II,” EH.Net, 2010.

The correlation between percentage increase in GDP and in federal spending is almost zero (-0.09). The correlation between percentage increase in GDP and defense spending as percentage of GDP is negative (-0.62). And the correlation between GDP percentage growth and defense spending percentage growth is -0.3. Neither the civilian nor the military Keynesian multiplier had any bearing on the growth of GDP and thus on the rise of the Welfare State. Contrary to common opinion, military expenditures are not the flywheel of economic growth.

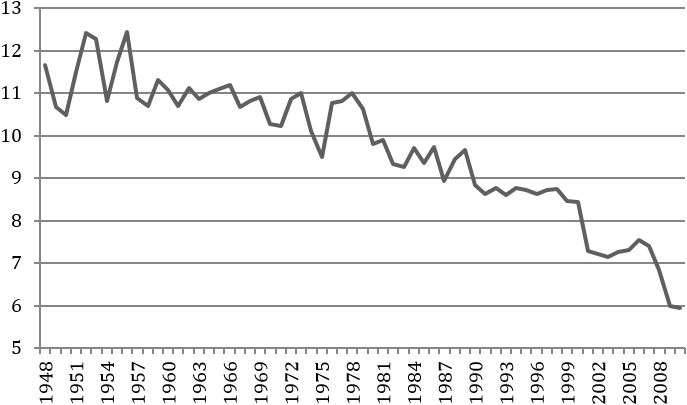

Similar conclusions are reached if debt is considered. The U.S. gross federal debt as a percentage of GDP decreased (rather than increasing) persistently during the Golden Age, from 121.7% in 1946 to 37.6% in 1970, as shown by Figure 6 below.

Figure 6: Gross Federal Debt (GFD) as a Percentage of GDP

Source: US Office of Management and Budget, historical tables, Table 7.1.

The long spell of prosperity was due neither to federal spending, either in the civilian or in the military sphere, nor to the federal debt. Rather, it was due to the reconversion, i.e. to the reconstitution of civilian capital, and to the liberation of pent-up purchasing power after the war. Greater supply was matched by greater demand.

There were also political and ideological factors (the Cold War, the anti-colonial and the anti-racist movement, etc.), which were favorable for a generalized pro-labour redistribution by capital. But redistribution does not generate economic growth. The quantity to be redistributed does not change due to redistribution. Economic growth, on the other hand, implies that the quantity to be redistributed grows before redistribution. Aside from the political context, the cause of the rise of the Welfare State was the powerful wave of economic growth following the reconstitution of the capitalist production relation and the liberation of the compressed purchasing power. Both wages and total profits rose. Expanded reproduction on a large scale made the Welfare State possible, not the other way around. But at the same time the fall in the average rate of profit both caused the crises in the Golden Age and undermined it.

The Fall of the Welfare State

The Golden Age lasted until around the mid-1970s. However, the ARP had started to fall much earlier, soon after the end of the War (Figures 3 and 5 above). This explains why the Golden Age was marred by six crises, two of which (in 1957-58 and in 1974-75) were particularly severe. Then, 15-20 years after the end of the War, the economy changed direction. The high economic growth (a rate of growth of new value of 3.7% and of total value of 3.9% from 1948 to 1979), high employment (a rate of growth of 42.2% in the same period) and the surge in mass consumption in the upward cycle hid the creeping economic malaise: the fall in the ARP. This is the reason why crises could mature and emerge within the context of a vigorous and protracted economic expansion. Crises are determined by falling profitability. The fall in profitability within the context of economic growth prepares the ground for the emergence of the downward cycle and of crises from within the upward cycle.

The rising organic composition started to bite into employment. The rate of unemployment rose from 4.9 percent in 1970 to 10 percent in 2010 according to the U3 measure (but 17 percent according to the U6 measure and 22 percent according to SGS estimates). High unemployment affected the rate of exploitation, which rose enormously especially with the advent of neoliberalism (see Figure 4 above). Both wages and the purchasing power accumulated during the war fell. The condition of the working class began to deteriorate and has been worsening ever since.

But before the effects of the falling ARP could emerge, 25 years went by. At that point, the long descent of the ARP that had begun right after the war put an end to the Golden Age and signed the beginning of the end of the Welfare State. The effects of the fall in the ARP had been merely postponed. It looked as if the new technologies had spurred the economy in the Golden Age. Actually, they increased labour’s productivity but were the major factor causing the shedding of labour. Far from increasing general profitability, they were the major force behind the long, secular increase in the organic composition and consequent fall in the ARP.

The widespread view that the economy started to deteriorate in the 1970s ignores that the ARP started to fall well before that time. This incubation, i.e. the progressive deterioration of profitability, was hidden by four factors: (a) labour’s higher productivity; (b) the technological leaders’ higher profitability; (c) the absorption of labour power by the expanded reproduction of the technological leaders; and (d) labour’s improved living conditions.

The fall in profitability in the upward phase was increasingly undermining economic growth from within because it was starting to reduce employment and thus the new value produced. Labour in the productive sectors reached its maximum strength in the 1970s. Employment reached its zenith in 1979 but the strength of labour began to decline earlier. The wage share was at its highest in 1973 (44.7%), after which it began to fall. As more firms closed down and unemployment could not be absorbed any longer by capital accumulation because of the consistent rise in the OCC, the second, downward phase set in.

Both labour and capital began to experience increasing difficulties in absorbing the rising output: the former because of falling employment and wages, the latter because of falling profitability. Difficulties of realization in the productive sectors began to emerge. Investment of capital in the financial sectors, where higher profit rates could be reaped, accelerated. The financial and speculative sectors ballooned. Financial crises started to emerge and became a recurrent feature. Capital had to reverse falling profitability. Around the mid-1980s capital unleashed a savage attack against an already weakened labour.16 Labour suffered an historic defeat. Austerity became the new buzzword. From 1986 to 2010 the wage share tumbled from 40.4% to 24.1%. Unfortunately, labour has not yet been able to reverse this trend.

A New Welfare State?

The long spell of pro-labour redistribution policies following the WWII failed to reverse the tendency for average profitability to fall. This was not due to wrong redistribution policies. Basically, high wages compress profits and profitability. Lower wages, on the other hand, increase profits and profitability. But by decreasing labour’s purchasing power, they also accentuate the difficulties of realization and thus dent profitability. Moreover, in the acute phase of the downward cycle (crises), profits are set aside as reserves and/or invested in finance and speculation, rather than in the production of value and surplus value. The speculative bubble inflates. Higher profits fail to revive the productive economy.

In sum, neither pro-labour nor pro-capital redistribution can halt or reverse falling profitability. Only sufficient capital destruction can do it. For the U.S. it meant a gigantic conversion of the civilian production relation to the military production relation without the destruction of the means of production and with full employment. For Europe, it meant the destruction of the civilian production relation following the destruction of the means of production and concomitant unemployment. In both cases, the Welfare State was the child of the rebuilding of the capital-labour relation in the civilian economy.

Capital cannot accept this analysis. For capital it is essential to believe that this system can be steered out of the recurrent crises and on the path of growth through adjustments in redistribution either in one sense or the other. Thus, faced by the failure of austerity (for labour) policies adopted since the 1980s, capital might resort to so-called ‘expansive’ measures. But lacking a powerful labour movement demanding radical redistribution measures, capital’s pro-labour policies will be of only limited scope, far from anything resembling a Welfare State.

The above has argued that Keynesian policies have not been responsible for the Welfare State. Rather, the root cause of the rise of the Welfare State has been a concomitance of exceptional circumstances: the reconstitution of the civilian economy (greater production of value) and the release of pent-up purchasing power (the absorption of that value). This concomitance has functioned as a temporary counter-measure to the increase in the organic composition of capital. The application of new war-related technologies to the civilian economy not only increased labour productivity significantly but also changed the ‘material structure’ of the economy. The exceptionality of the Golden Age is the reason why high growth and high employment could coexist with a falling ARP for more than two decades. The Welfare State was possible because of a vigorous and sustained economic growth such that both wages and profits could grow. The present situation is in no way close to it. Employment and new value have been falling since 1979.

The condition necessary but not sufficient for a new Welfare State would be the previous destruction of capital, a destruction comparable to, or perhaps even greater than, the conversion of the civilian economy into a war economy and then again into a civilian economy in the U.S. and in Europe. This might mean another global war. Or a world-wide, truly fundamental capitalist change whose modalities and outcome are impossible to preview at this stage. Or perhaps the world economy will slide into a long and protracted state of stagnation. But the latter would not be capitalism any longer. Capitalism is by definition a dynamic system. These hypotheses are speculative. But none of them can be ruled out a priori.

There is a similarity, though, between the rise of the Welfare State in the past century and the present: new technologies, which were developed towards the end of the 20th century and which wait to be implemented on a large scale across the entire spectrum of the economy. Let us mention some of them: biotechnology, genetic engineering, nanotechnology (the attempt to control matter on a molecular scale); bioinformatics (the application of information technology and computer science to the field of molecular biology); genomics (the determination of the entire DNA sequence of organisms); biopharmacology (the study of drugs produced using biotechnology); molecular computing (computational schemes which use individual atoms or molecules as a means of solving computational problems); and biomimetics (the science of copying life, i.e. the transfer of ideas from biology to technology). The widespread application of these technologies will trigger another revolution in the “material basis” of society, which will change it beyond recognition. But within the capitalist production relations, it will give rise to new and even more terrible forms of exploitation without eradicating the root cause of crises and of all the miseries afflicting the vast majority of the world population.

This, of course, assumes that capitalism will avoid a major ecological catastrophe and/or a new world conflagration, which would threaten the survival of humankind. Marx once said that history repeats itself, the second time as a farce. This time it might be not a farce but an immense and irreversible tragedy.

References

CaÏmara Izquierdo, S. “The dynamics of the profit rate in Spain.” Review of Radical Political Economics 39:4 (2007): 543-561.

CaÏmara Izquierdo S. “Short and long-term dynamics of the U.S. profit rate in the context of the current crisis.” Paper presented at the Congrès Marx International VI ‘Crises, Révoltes, Utopies’, Université de Paris-Ouest-Nanterre-La Défense, France (22–25 September, 2010).

Carchedi, G. Behind the Crisis: Marx’s Dialectics of Value and Knowledge. Leiden: Brill, 2011.

Carchedi, G. “Could Keynes end the slump? Introducing the Marxist multiplier.” International Socialism 136 (2012). Available at: http://isj.org.uk/could-keynes-end-the-slump-introducing-the-marxist-multiplier/.

Carchedi, G. “The Law of Crises.” In G. Carchedi and M. Roberts, eds., The World in Crisis. Zero Books: 2017.

Harvey, D. The Enigma of Capital: And the Crises of Capitalism. Oxford University Press, 2010.

Jones, P. “Depreciation, Devaluation and the Rate of Profit.” Paper presented at the the WAPE/AHE/IIPPE conference (2012).

Maito, E. E. “Income distribution, turnover speed and profit rate in Chile, Japan, Netherlands and United States.” MPRA Paper No. 59283 (2014). Available at: https://mpra.ub.uni-muenchen.de/59283/.

Maniatis, T. and Passas, C. “Profitability, Capital Accumulation and Crisis in the Greek Economy 1958–2009: a Marxist Analysis.” Review of Political Economy 25:4 (2013): 624-649.

Marquetti, A., Filho, E. M., and Lautert, V. “The Profit Rate in Brazil, 1953-2003.” Review of Radical Political Economics 42:4 (2010): 485-504.

Marx, K. Capital, Vol. 2. New York: International Publishers, 1967.

Milward, A. S. War, Economy and Society, 1939-1945. Berkeley: University of California Press, 1977.

Norfield, T. “Derivatives and Capitalist Markets: The Speculative Heart of Capital.” Historical Materialism 20:1 (2012): 103-132.

Ritschl, A. “The Marshall Plan, 1948-1951.” EH.Net (2008). Available at: https://eh.net/encyclopedia/the-marshall-plan-1948-1951/.

Tassava, C. “The American Economy during World War II.” EH.Net (2010). Available at: http://eh.net/encyclopedia/article/tassava/.

Notes

- The data considered in this paper comprise agriculture, mining, construction, and manufacturing. Services can be either productive or not, but official data are not suited to separate the productive from the unproductive activities. See G. Carchedi, (2011).

- Wages are called variable capital because they are spent for labour-power, that generates more value than its own value. The capital spent on the means of production is constant because the means of production do not produce value and thus cannot generate more value than their own value. Their value is transferred to the value of the product.

- A the more precise formulation would have to introduce the equalization of the profit rates. But the conclusion would remain the same.

- T. Norfield (2012), for US data; S. Cámara Izquierdo (2007), for US data;; P. Jones (2012), for US data; E. Maito (2014), for core countries; T. Maniatis and C. Passas (2013), for Greece; A. Marquetti, E. Filho, V. Lautert (2010), for Brazil also find a downward trend in the rate of profit starting approximately from the end of WWII. These works will be published in G. Carchedi and M. Roberts (eds.), The World in Crisis (Zero Books: 2017), forthcoming. But for other authors the ARP rises tendentially up to the 1970s and starts falling afterward. This raises the question whether a long and protracted period of rising profitability can be the humus from which crises can emerge. See G. Carchedi, “The Law of Crises,” in The World in Crisis (Zero Books: 2017), forthcoming.

- In the US the destruction of capital was the destruction of the capitalist production relation while the means of production and labour-power were not only unscathed but actually were fully employed. In Europe, the destruction of the means of production and labour-power determined the destruction of the capitalist production relation.

- “Table 5.2.3: Real Gross and Net Domestic Investment by Major Type, Quantity indexes,” Bureau of Economic Analysis (BEA), available at: http://www.bea.gov/iTable/iTable.cfm?ReqID=9&step=1#reqid=9&step=3&isuri=1&910=X&911=0&903=138&904=1940&905=2011&906=Q.

- A. Milward (1977), p. 236.

- A. Milward (1977), p. 229. The shortage of male industrial workers (10 million were absorbed by the war effort) was made good by the proletarianization of agricultural labour and by the influx of women in the labour process.

- Of course, the military industry keeps playing an important role in the US, but not because it raises profitability but because it is necessary for imperialist expansionism and thus for the appropriation of international value and surplus-value.

- D. Harvey (2010), p.169.

- K. Marx (1967), p. 186).

- The literature focuses also on a number of other aims, especially political. For a review, see A. Ritschl (2008).

- The question is which industries and individuals benefited ($3.5 billion was spent on raw materials; $3.2 billion on food, feed and fertiliser; $1.9 billion on machinery and vehicles; $1.6 billion on fuel) and which corporations. General Motors got $5.5 million worth of orders between 1950 and 1951 and Ford Motor Company got $1 million. The biggest beneficiary was Anderson, Clayton & Co, with $10 million of orders up to the summer of 1949. William Clayton, the co-owner of this firm and the under-secretary for economic affairs toured Europe and played a key role in preparing the plan, which he pushed through Congress, personally benefiting to the tune of $700,000 a year.

- A. Ritschl (2008).

- G. Carchedi (2012).

- The ideological weakening of labour is one of the major causes of labour’s defeat.